MSFT has $25B eaten by memory. Samsung HBM4 sold out. KLA Korea +80%. QCOM auto +38%. Corning: two more hyperscaler optics deals. Softbank Robotics IPO?

Microsoft, Meta, Alphabet, and Amazon all reported accelerating cloud growth, raised or held CapEx commitments, and pointed to the same problem. Can you guess? Yep, the skyrocketing price of memory.

Hyperscalers get all the talk, but what about the suppliers cashing those checks? Samsung had earnings and mentioned sold out HBM4 capacity. KLA’s Korea revenue jumped 80% YoY… because memory. Corning added two more multi-year hyperscaler LTAs on a scale comparable to its $6B Meta agreement.

Also, Qualcomm’s automotive biz is doing great (as we expected yesterday). But everyone’s talking about Qualcomm’s surprise custom ASIC mention.

Oh yeah, lastly, SoftBank is plotting a robotics IPO! Say what?

Let’s get into it.

— Austin & Vik

Austin: Vik is back from vacation next week, so expect even better updates ahead!

Hyperscalers feeling the pinch

Hyperscalers are increasing CapEx, not just for more accelerators but to pay for rising component costs.

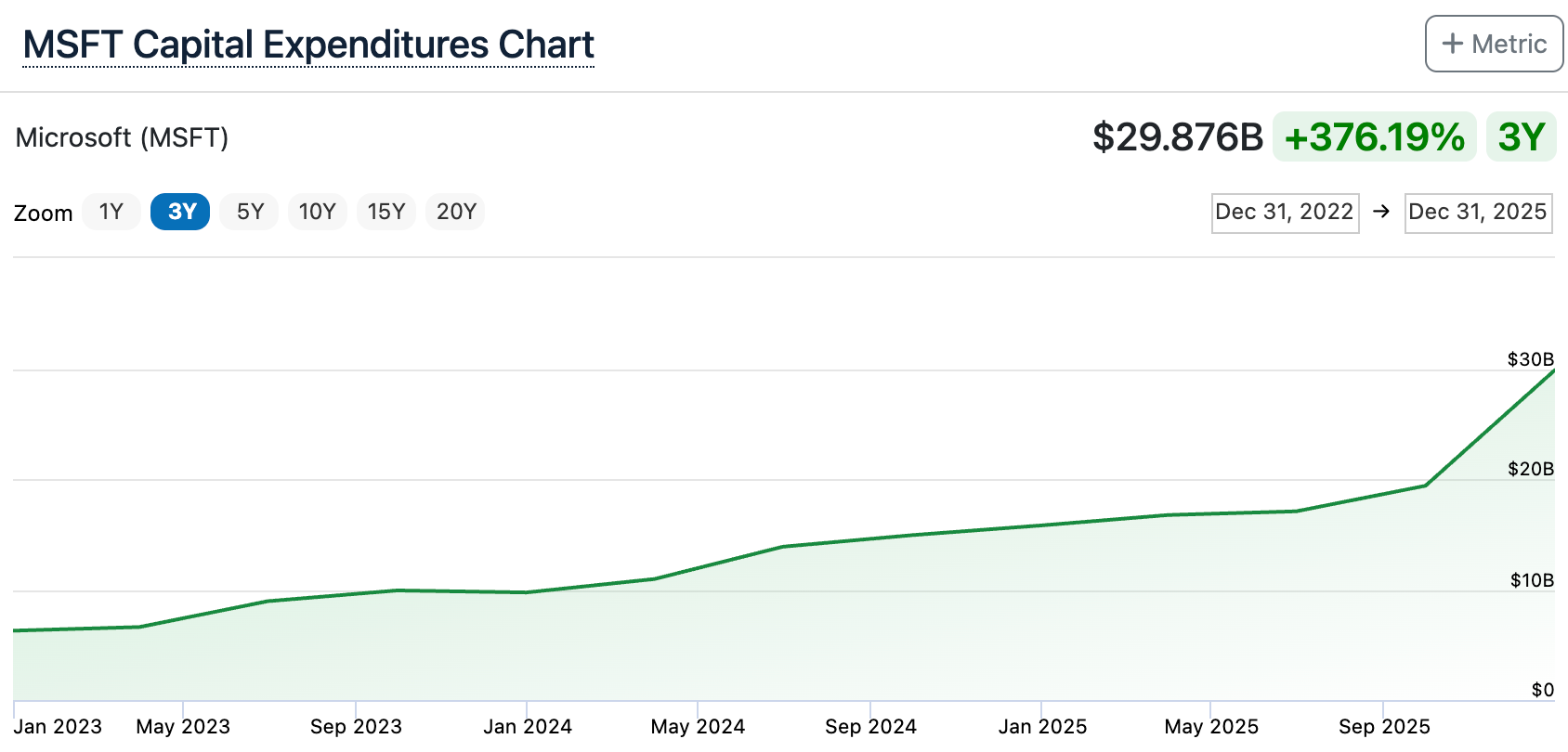

Microsoft’s increasing CapEx another $40B. CFO Amy Hood attributed roughly $25B of calendar 2026 CapEx specifically to higher component pricing(!!!), and said capacity stays tight at least through 2026 even with Fairwater Wisconsin coming online six weeks early. (Microsoft IR)

Meta raised 2026 CapEx to $125–145B from a prior $115–135B, citing “higher component pricing this year and, to a lesser extent, additional data center costs to support future year capacity.” CFO Susan Li said Meta has “continued to underestimate our compute needs even as we have been ramping capacity significantly.” (Meta IR)

Alphabet posted Google Cloud at $20.0B, up 63% year-over-year (!!!), with operating margin expanding from 23.7% two quarters ago to 33%. Sundar Pichai said cloud revenue “would have been higher if we were able to meet the demand”.

AWS reaccelerated to 28% growth on $37.6B revenue with operating margin at 37.7%, up from 34.7% the prior quarter. CEO Andy Jassy said “At scale, we expect Trainium will save us tens of billions of dollars of CapEx each year and provide several hundred basis points of operating margin advantage versus relying on others’ chips for inference.”

Austin: Yeah, we all knew memory and storage pricing would hit the hyperscalers hard, but still… pretty crazy to see the numbers. Microsoft indicated that $25B of the $40B CapEx increase is due to component pricing. Ouch!

$25B is more than MSFT spent per quarter in CapEx until recently!

Also, I’m updating my priors on Amazon. Read here.

AWS Trainium at $20B run rate, “largely sold out”

Andy Jassy disclosed Trainium at a $20B annualized run rate growing triple digits, with Trainium2 “largely sold out” and Trainium3 “nearly fully subscribed.” He said Trainium would save AWS tens of billions of dollars of CapEx savings per year and several hundred basis points of operating margin advantage on inference vs. merchant chips.

Austin: Tens of billions of dollars of CapEx savings is awesome… until you spend all that savings on skyrocketing memory and storage 😭. But in all seriousness, good for the Trainium team. We need to get them on a Semi Doped pod to talk more.

Also, I’m changing my tune on Amazon: https://www.chipstrat.com/p/rethinking-amazon-not-all-saas-is

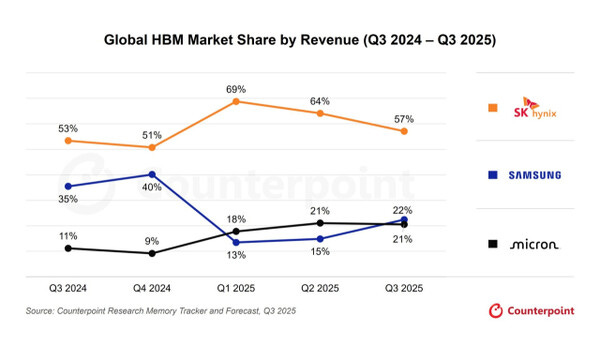

Memory: Samsung’s making bank on the receiving end, says server demand stays strong

Samsung’s AI memory carries the print.Go figure. The hyperscalers just told us how expensive memory is…

Samsung is a beneficiary. The earnings release says we can expect more of the same for second half: “In H2 2026, the Company expects server memory demand to remain strong as hyperscalers accommodate enterprises’ increasing adoption of AI and LLM services.” (Samsung Newsroom)

Austin: There was also a lot of HBM4 talk on the call.

On timing, Samsung claims they are first to ship HBM4 “after we became the world’s first to commence commercial shipment of HBM4 in February”.

They also believe their HBM4 is differentiated by it’s performance, leading to pricing power and a sold out backlog: “The differentiated performance of our HBM4 led to concentration of demand and our production-ready capacity is fully booked and sold out…As customers adopt these enhanced specifications, our outstanding performance has been translating into actual premium on pricing.”

And they aren’t done yet, next-gen HBM4E samples in Q2: “accelerating development of next-gen HBM4E products with pin speed of 16 Gbps and bandwidth of 4.0 terabytes per second with samples set to start shipping within the second quarter”.

The talk is quite confident like they’re on a comeback. They have a lot of ground to try and recover.

But Micron’s not going to just sit by and give market share back…

KLA: Korea +80%, advanced packaging raised again

KLA confirmed the fab CapEx is being deployed, not just ordered. Q3 FY26 results posted Korea revenue up 80% year-over-year, while Taiwan declined 12%. Management raised the calendar 2025 advanced packaging revenue guide again to over $925M, and pegged KLA’s share at roughly 6% of an $11B market versus 1% a few years ago. Services revenue grew 16% to $775M — the installed-base tell on fab utilization at TSMC, Samsung, and Intel. (KLA IR)

Austin: Korea way up. Samsung is in Korea. So is SK hynix. Oh yeah, and the hyperscalers are spending like crazy on memory. KLA confirmed it on the call too. HBM is driving 50% YoY DRAM process control growth.

Fabs are busy, man. Tools getting installed (Korea +80%), tools getting serviced (services +16%), wafers shipping at the leading edge, and advanced packaging revenue raised again to north of $925M. logic + memory + advanced packaging + services. Nice.

Corning lands two more hyperscaler optical LTAs

Don’t forget Corning, who reported a few days ago too. On the call, CEO Wendell Weeks confirmed two additional multi-year hyperscaler agreements similar in size to the up-to-$6B Meta deal disclosed earlier. Weeks framed pricing as “clearly favorable for those who have capacity.” (Corning IR)

Austin: Ahhh… when hyperscalers say “component pricing increases”, that means more than just memory and storage. I didn’t even think about fiber tbh.

Although, to be fair, the CEO had a great quote on the call talking about innovating to deliver more value and cost savings to the customer, and then sharing in that savings:

“CEO Wendell Weeks: Second, you are correct that the pricing environment is clearly favorable for those who have capacity. Our approach to increasing our profitability, though, comes primarily from how do we uniquely innovate and how do we uniquely manufacture our products rather than focusing on price increases of commodity-based products. So what we try to do here is we’re introducing these new innovations that we hear our customers talk about and hear us talk about. And what they do is they create more value for our customers by reducing their total installed cost. And then we share that value creation with them, which increases our profitability much more rapidly and sustainably over time than simply capturing any particular near-term move, whether it be on bare fiber or loose tube cable or anything like that”

Austin: That’s the right mindset imo. Of course, I’d love to talk to customers and confirm if they feel same way. I have a feeling the statement is genuine, in part because Corning is 175 years old, and companies that last that long usually have an incredible customer-centric mindset.

Qualcomm’s auto: $1.33B at +38% YoY, Q3 guide ~50%

Auto is the most exciting Qualcomm growth story, even with hints of datacenter and custom silicon mentioned on the call. Q2 FY26 auto revenue hit $1.33B, up 38% year-over-year, with Q3 guided to roughly 50% growth and an exit run rate above $6B. Cristiano Amon described the fifth-gen Snapdragon Digital Chassis as the largest gen-over-gen content increase in company history.

Austin: Qualcomm is building a legit automotive franchise. See my primer from this time last year. Drivers want better in-cabin digital experiences and increasingly ADAS, both of which require connectivity. All tailwinds for QCOM.

Not every vehicle can carry a flagship digital experience, though. And QCOM Snapdragon Ride has a portfolio that scales from entry to premium, so OEMs match silicon to price point. Design wins span Europe, Asia, and America.

This quarter’s $1.33B auto revenue at +38% YoY, with Q3 guided to ~50% growth and an exit run rate above $6B, is the receipt. I think Qualcomm’s automotive biz is for real.

Japan + robotics makes sense SoftBank + datacenters is a thing (Stargate) SoftBank recently acquired the industrial robotics business from ABB SoftBank had, at one time, owned Boston Dynamics.

I can squint and see all of this coming together… Japan, robotics, datacenters, SoftBank.

But IPO talk already? Really?

Oh, one more interesting bit from the WSJ article: Bilal Safeer, an executive at SoftBank-owned Arm, is currently serving as interim CFO of the venture.

Looking Ahead

The fun doesn’t stop. Apple, MediaTek, Sandisk, Western Digital, and Rivian all report today.