First things first. Both Austin and Vik will be at Computex 2026 in Taipei next week. If you see them, stop and say hi. Will try to keep posting daily updates.

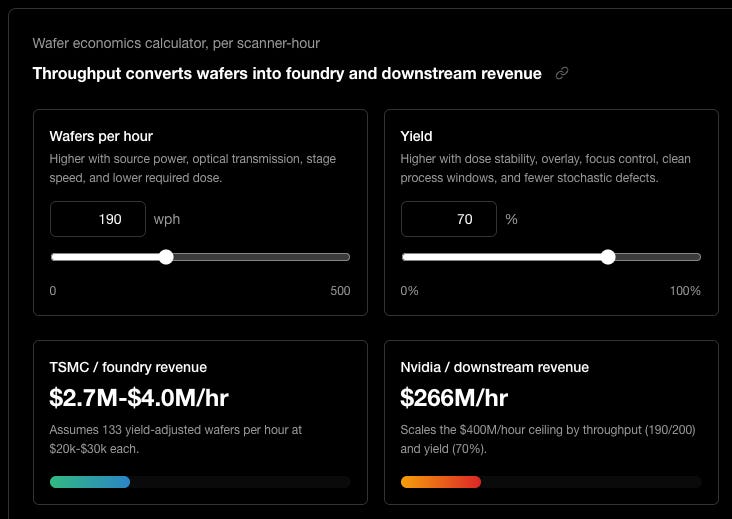

More importantly, and this is the downright most flattering thing that has ever happened to Semi Doped. Noam Hurwitz was inspired to start blogging again after listening to our Masterclass on Lithography episode, and decided to write an absolutely sick interactive article with dashboards and all the bells and whistles. You can move sliders around and see how everything changes!

If you ever enjoy our content, reply/DM and let us know. Be like Noam.

Ok, now on to the today’s greatest hits! Good things await.

Quick hits, high signal. Takes from semi industry experts. Sign up for free daily updates!

Be sure to check out the Semi Doped podcast on YouTube or your favorite podcast player!

TSMC reportedly eyes 15% 3nm price hike in 2H26, +5-10% in 2027 amid AI demand

TSMC is expected to raise 3nm wafer pricing by up to 15% in 2H26, with an additional 5-10% increase in 2027. Fab 18 monthly 3nm capacity climbed from ~130,000 wafers in early 2026 to 160,000-175,000 in Q2, but the report says AI demand growth continues to outpace the ramp.

3nm demand has flipped from smartphone-led to AI-led. Nvidia, AMD, Google, AWS, and other cloud customers are accelerating 3nm adoption for AI server refresh cycles and in-house ASIC programs. Institutional investors quoted in the report describe 3nm as the most stable mass-production node for AI chips, with better maturity than 2nm, which is still ramping yield. Per Liberty Times, Nvidia GPUs, Broadcom ASICs, and Marvell custom chips remain heavily dependent on TSMC. TrendForce estimates TSMC’s global foundry market share at 70.4% in 4Q25.

C.C. Wei is expected to address AI demand, advanced-node capacity, and overseas expansion at TSMC’s annual shareholder meeting on June 4. At a May 26 dinner with Jensen Huang, when asked whether TSMC could meet Nvidia’s capacity requirements, Wei replied, “we’re already working very hard” while making a zipper-across-the-mouth gesture. Huang referred to TSMC as “my good friends.” (TrendForce via Commercial Times)

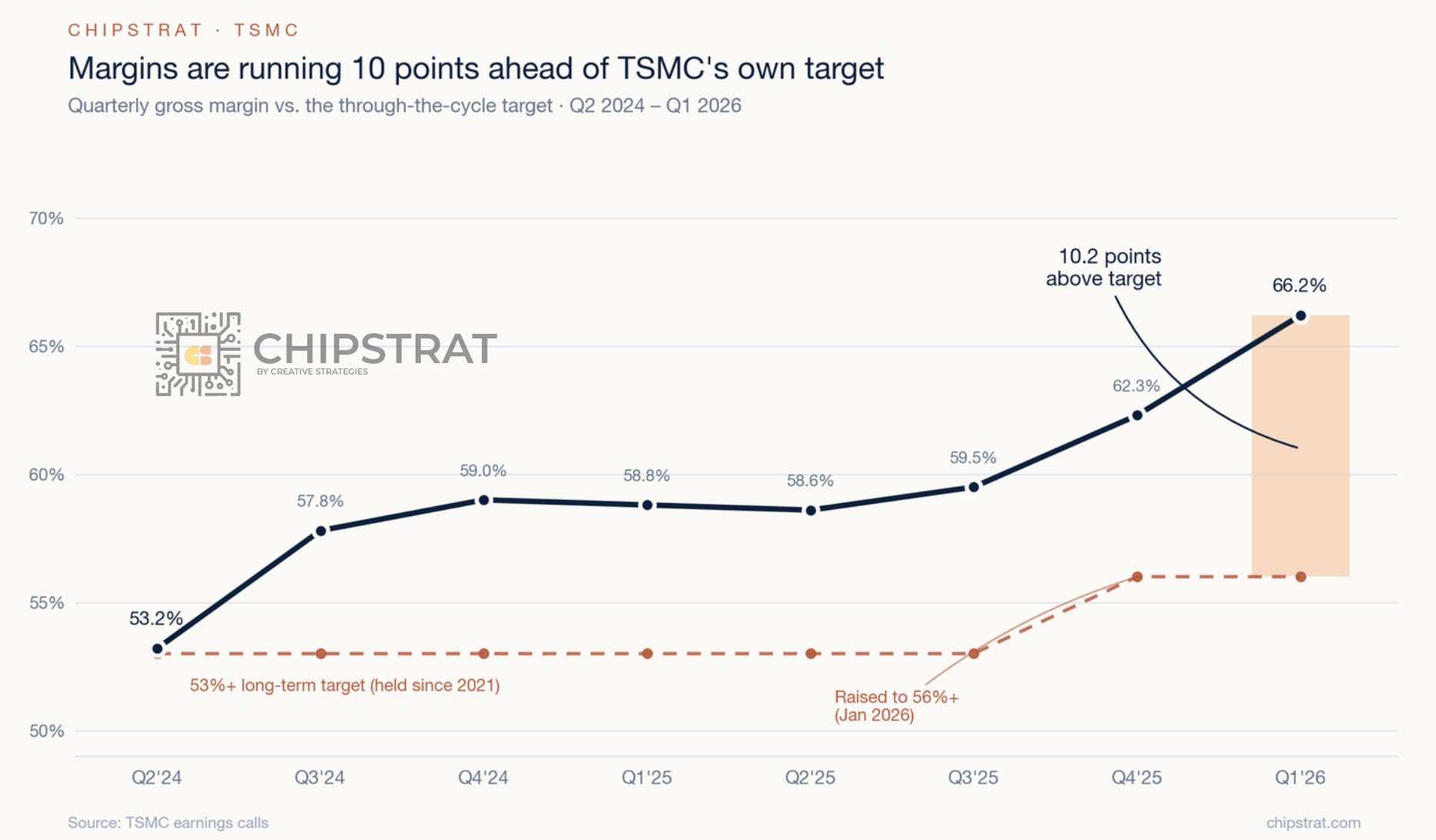

Austin: TSMC can embrace a value-based pricing model, rather than a traditional “cost-plus” manufacturing pricing model. Which is a fancy way to say they have pricing power and a differentiated, premium product. We see this in margins, which are running way ahead of forecasted targets:

The question is, what is the true value of a 3nm wafer? It’s surely even more than what TSMC is asking even after price hikes. imo this is all a function of not enough supply…

Vik: Intel 18A capacity couldn’t come sooner. The world needs you Intel. Lip-Bu, we’re counting on you dude.

Marvell raises FY28 data center target by $1.5B to $16.5B as custom XPU “more than doubles” next year

Marvell reported Q1 FY27 net revenue of $2.41B, up 28% YoY, and guided Q2 to $2.67B ± 5%. Management raised the FY28 target by $1.5B to $16.5B and said custom silicon will more than double, split evenly across existing programs, XPU attach, and new tier-1 wins. All three buckets sized up since last quarter. CEO Matt Murphy held the $10B+ custom silicon goal against a $55B FY29 TAM.

CFO Willem Meintjes broke out scale-up optics (NPO/CPO) as a new ~$300M revenue line, calling it “Gen 1, ground zero.” The Polariton tuck-in adds plasmonic modulators with a claimed 10x bandwidth headroom on top of the Innovium scale-up switching base.

President Chris Koopmans said “everything that touches AI has been constrained since the beginning.” Marvell has put roughly $1B of supplier prepayments out this fiscal year and is now giving 5-year forecasts to lock capacity. Interconnect growth expectations have moved from 30% to 50% to 70%+ across three quarters. (Marvell IR)

Austin:How did I miss the Polariton acquisition!? Plasmonics! I had an amazing professor during undergrad who taught my “Electromagnetic Fields and Waves” course and his research focus was plasmonics. It was honestly over my head at the time, but I remember he was a fantastic artist and could draw amazing 3D images on the chalkboard (do they still have those anymore?)

Vik: Austin, you’re not reading my TWiC columns man. Scale-up optics is getting more real, with more InP orders coming in than the industry can handle. Polariton is Marvell bet for 3.2T networking.

Synopsys Q2 2026 +42% YoY, Elliott settles for a board seat

Synopsys reported Q2 revenue of $2.28B, up 42% YoY (quarter ended April). Shares fell 1.6% to $525.92 Wednesday and another 2.1% after the close. SNPS filed its 10-Q, Q2 transcript, and two 8-Ks the same day.

Synopsys also settled with Elliott Investment Management. Elliott managing partner Jesse Cohn joins the SNPS board on June 1, with a seat on the corporate governance and nominating committee, expanding the board to 11. Elliott agreed to standstill and voting commitments. Elliott disclosed a multibillion-dollar SNPS stake in March 2026, citing revenue growth that had trailed expectations despite the company’s EDA market lead.

“As an experienced board member, Jesse brings a uniquely differentiated perspective,” Aart de Geus, executive chair and founder of Synopsys, said in the statement Wednesday. (Bloomberg)

Austin:If you’re curious about the activist investor, Sassine addressed it well in the call during prepared remarks and the Q&A.

Dell raises forecasts on AI server demand

Dell lifted its fiscal 2027 forecasts, guiding to roughly $60 billion in AI server revenue and citing customer count above 5,000 across neocloud, sovereign, and enterprise buyers. Q1 AI server revenue came in at $16.1 billion, above the $14.6 billion quarterly run-rate implied by the full-year guide, with management attributing a back-half deceleration to supply constraints on DRAM, NAND, and CPUs rather than demand. COO Jeff Clarke said customer discussions now span three to five years, driven by access to supply. Shares rose about 38% in after-hours trading following the report. (Reuters)

Vik: Damn, first SNOW 0.00%↑ goes up 30%+, then DELL 0.00%↑ again another 30%. IN THE SAME WEEK!

Quick Hits

Foxconn projects 10,000 CPO switch trays in 2026 (@jukan05)

BYD debuted an in-house smart-driving chip that the Chinese automaker described as the country’s most powerful, marking the company’s first proprietary silicon for advanced driver-assistance systems. (Bloomberg Tech)

EXTOLL and Chip Interfaces unveiled what they call the industry’s first UCIe IP solution for GlobalFoundries FDX technology, enabling chiplet integration on FD-SOI nodes. (GlobalFoundries)

Nvidia Research detailed advances moving robotics from simulation to real-world deployment, pushing generalizable embodied autonomy across its Isaac and GR00T robotics stack. (Nvidia News)

Cerebras requires 24 systems and roughly $24M capex to run a single deep coding model at max context, supporting only 256 concurrent users per cluster. (X (@SemiAnalysis_))

Key Data

How much money a $20/mo makes for the model provider, depends on how much of your quota you use. So Anthropic revenue going to the moon means people got an AI sub, but haven’t figured out how to use it yet? What happens when they do?

via SemiAnalysis on X.

Thanks for reading! This post is public so feel free to share it.

As someone who is from Taiwan, it is such a GREAT honor to have you guys come here and visit COMPUTEX!! Travel safe and have the best time ! 🙏Highly recommended trying bubble milk tea 🧋 and visiting Taipei 101 😆

As someone who is from Taiwan, it is such a GREAT honor to have you guys come here and visit COMPUTEX!! Travel safe and have the best time ! 🙏Highly recommended trying bubble milk tea 🧋 and visiting Taipei 101 😆